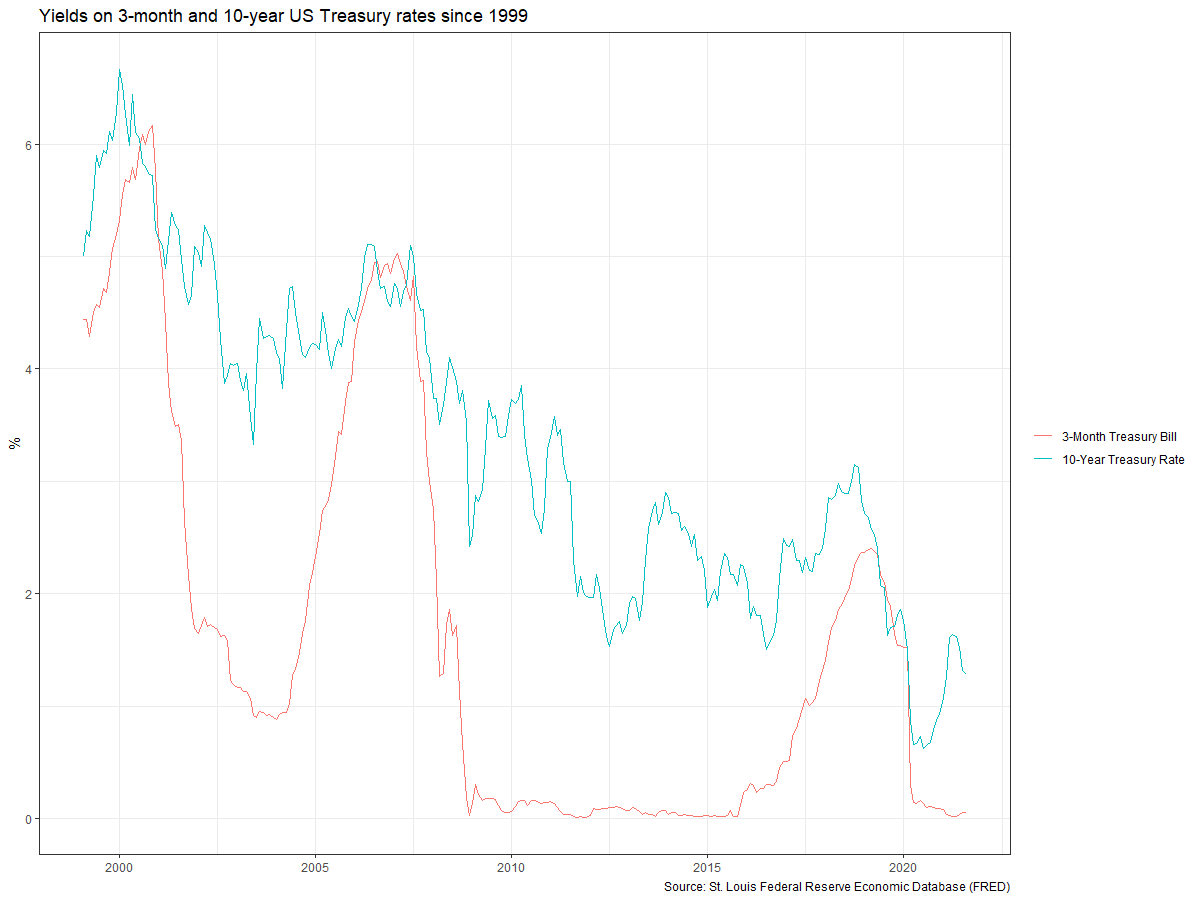

recessions_yc <- yield_curve %>% # Filter for 3m and 10y maturities and select years from 1999

filter(maturity %in% c("3m","10y")) %>%

filter(year(date) %in% c(1999:2021))

# plot the yields on 3-month and 10-year US Treasury rates since 1999

ggplot(recessions_yc, aes(x=date, y=value, colour=duration)) +

geom_line() +

theme_bw() +

theme(legend.title = element_blank()) +

scale_color_manual(values = c("cadetblue3", "pink")) +

labs(

title = "Yields on 3-month and 10-year US Treasury rates since 1999",

y="%",

x="",

caption="Source: St Louis Federal Reserve Economic Database (FRED)")